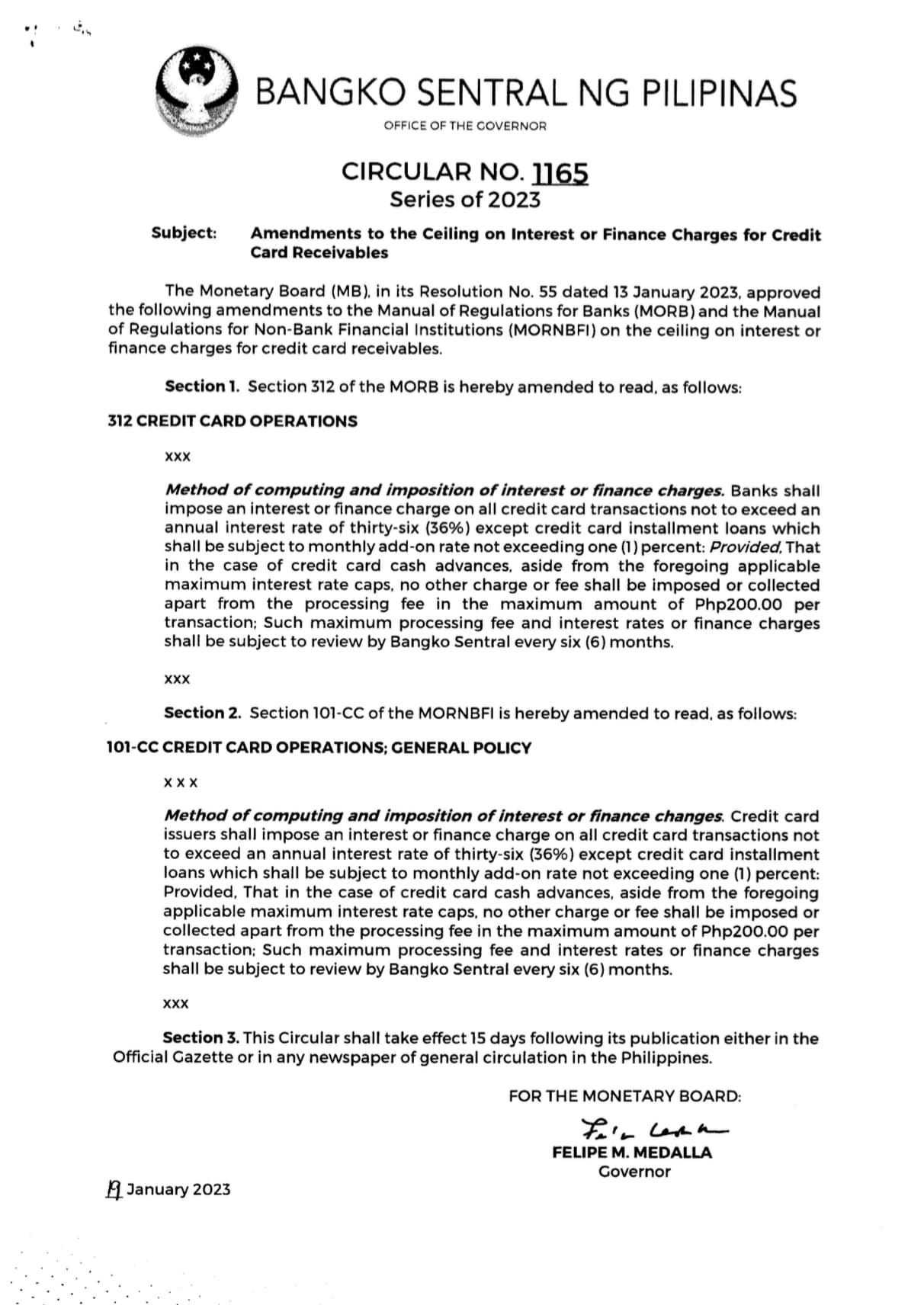

The recent circular approved by the Monetary Board gave way in setting a ceiling for interest rates for banks for both secured and unsecured loans to 3% per month. The banks on the other hand went giddy and immediately announced to their customers that they are increasing the interest rate per month to 3%.

The circular is not their license to make an increase. The Supreme Court time and again ruled that a 3% interest rate is excessive, iniquitous, and unconscionable. In Macalinao vs BPI, (G.R. No. 175490), it was held by the Court:

While C.B. Circular No. 905-82, which took effect on January 1, 1983, effectively removed the ceiling on interest rates for both secured and unsecured loans, regardless of maturity, nothing in the said circular could possibly be read as granting carte blanche authority to lenders to raise interest rates to levels which would either enslave their borrowers or lead to a hemorrhaging of their assets.

This means that during this time that the Central Bank Circular removed the ceiling, it does not mean that banks can raise their interest rates that would burden their borrowers. More so in this that they have set a ceiling of 3%.

Being excessive, iniquitous, and unconscionable means that a contract stipulation in this setting is void.

Article 1306 of the New Civil Code provides that “[t]he contracting parties may establish such stipulations, clauses, terms and conditions as they may deem convenient, provided they are not contrary to law, morals, good customs, public order, or public policy.”

In the case of Rivera vs. Spouses Chua, the court held that a 5% interest per month or 60% interest per year is unreasonable and iniquitous and thus void. Having a void stipulation for the contract, the rate of interest was set to 12% per year in this case from the date of judicial or extrajudicial demand. The 36% interest per year or 3% per month under the new BSP circular falls within the same blanket. This circular has no support in law, principles of justice, or in human conscience. And so, the new impositions of banks cannot prevail once it reaches the courts.